Silicon Valley’s $30B Bet on 63 Frontier AI Labs

On May 6, 2026, Deedy Das — Partner at Menlo Ventures (@deedydas) — published an evolving market map he’s compiled since November 2025. The post is brief, but the list is exhaustive:

The Rise of Neolabs

This cohort of 63 startups commands a combined valuation of ~$30 billion — all pre-product-market-fit (PMF), nearly all pre-revenue, and virtually all valued at unicorn level or higher.

They are collectively termed Neolabs: next-generation AI research laboratories founded by elite researchers, professors, or financially independent entrepreneurs from top-tier AI labs.

What defines a Neolab?

According to Deedy Das: A Neolab is an AI research lab — typically founded by ex-frontier-lab researchers, professors, or self-funded entrepreneurs — operating pre-PMF and with minimal revenue, yet raising unicorn-plus valuations to pursue long-term breakthroughs.

Among the top 10 tracked Neolabs, nine raised seed rounds exceeding $1B, despite annual revenues under $10M. Most founders are former OpenAI, DeepMind, or Anthropic leads — many already worth $10M–$100M+.

In their view, launching a 10M-MAU app is mediocre. Building models capable of rewriting mathematical logic or altering our understanding of physical laws? That’s the only defensible moat.

We’re entering an era where research is product, and capability is valuation.

Notable Neolab Highlights

- Roze (~$100B, 2026, Robotics): SoftBank’s meticulously orchestrated AI/robotics IPO vehicle — focused on robot-built data centers.

- Thinking Machines Lab (~$50B, 2025, Frontier Research): Founded by Mira Murati (ex-OpenAI CTO); holds the largest seed round in Silicon Valley history.

- Project Prometheus (> $38B, 2025, Robotics): Jeff Bezos’ bet on embodied AI in the physical economy.

- SSI / Safe Superintelligence ($32B, 2024, Frontier Lab): Ilya Sutskever’s ultra-secretive, pure-research lab — no roadmap, no product, maximum opacity.

- Reflection AI (> $25B, 2024): Ex-DeepMind team distributing open-source frontier models.

- Skild AI, Physical Intelligence, Periodic Labs, World Labs, AMI Labs, Inflection AI, Hark, Recursive Superintelligence: Valued between $4B–$15B; nearly all founded post-2024.

- Sooth Labs: The lowest entry threshold — $335M — still qualifying for inclusion.

Ilya Sutskever, Paul Christiano, Daniel Kokotajlo (L–R)

Why Neolabs Matter: Lessons from Anthropic

“Why does this wave matter?”

Because Anthropic was once a Neolab.

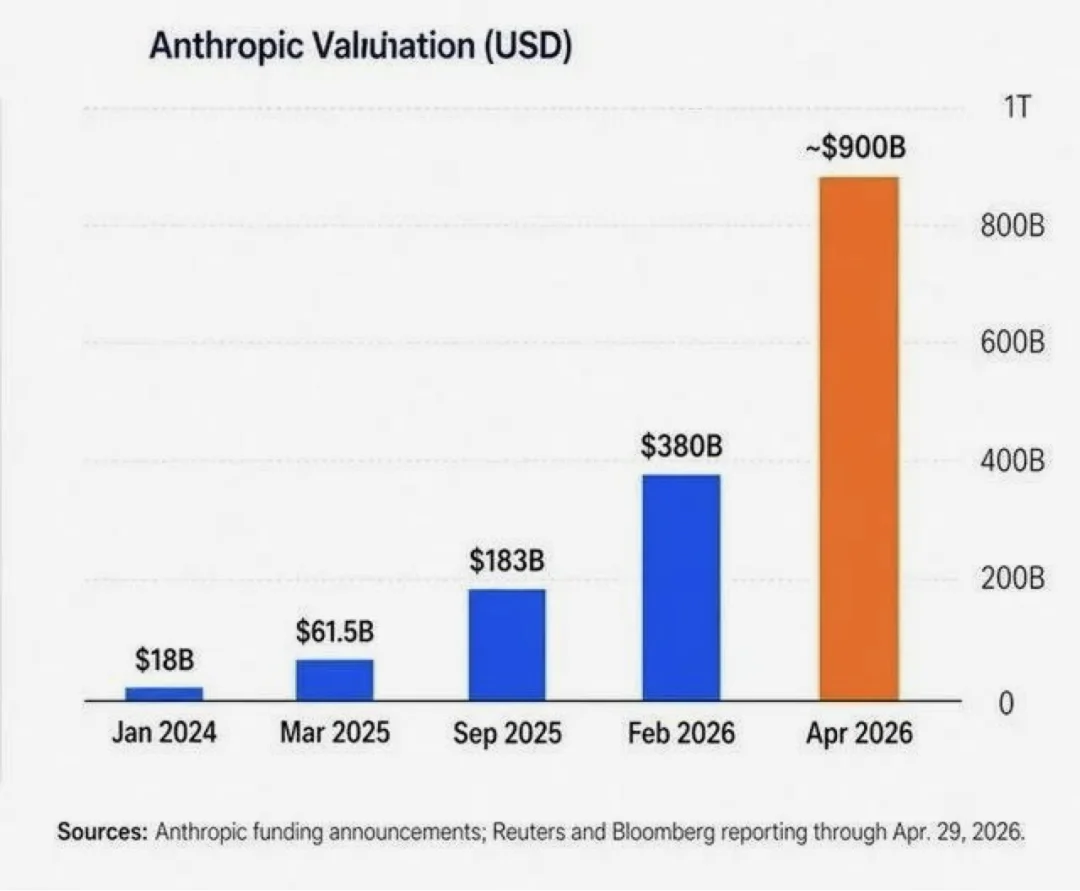

Founded in 2021 by Dario and Daniela Amodei after their departure from OpenAI — driven by divergent views on AI safety and alignment — Anthropic raised unicorn-level capital before shipping any product. It spent two years in deep R&D before launching Claude.

By 2026, its ARR hit $30B, and its valuation is projected to surpass OpenAI’s in H2.

Anthropic’s valuation trajectory (2021–2026)

If you’d dismissed Anthropic in 2021 with: “Just another GPT derivative — no product, no moat, talent will leak back,” you’d have missed one of the decade’s greatest opportunities.

So why do investors back today’s Neolabs? Three core rationales:

1. Pattern Recognition Across Paradigm Shifts

Every major tech paradigm spawns a wave of seemingly irrational pre-revenue valuations — until winners emerge.

- Internet → Amazon, Google, Salesforce (95% failed)

- Mobile → Uber, Instagram, WhatsApp (vast majority failed)

The asymmetry? Survivors are so massive they justify the entire portfolio.

Today, OpenAI + Anthropic alone sit at $500B–$1T combined. Just one Neolab achieving that scale would more than recoup the $30B total invested.

That’s not betting on companies — it’s betting on the category.

2. Structural Shift: AI as General-Purpose Technology

If AI is truly a general-purpose technology — comparable to electricity or the internal combustion engine — then we’re likely in the first 10% of its economic impact.

Even if most Neolabs fail, current valuations may still be too low, relative to the ultimate value of native-AI companies.

Here’s a novel framing rarely used in media:

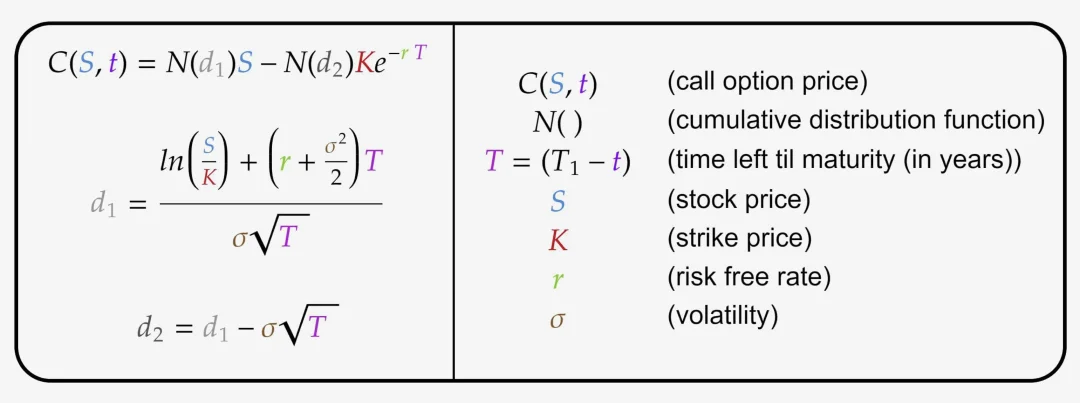

Neolabs are options — not equity.

When you write a $1M check at a $1B seed valuation, you’re not buying meaningful operational equity. You’re buying an option: the right (but not obligation) to participate in a future breakthrough — contingent on the team delivering foundational research progress within ~18–36 months.

- Strike price: Next-round valuation

- Expiration: ~2–3 years

- Underlying volatility: Extreme — most options expire worthless; a few yield $10B+ returns.

Three implications follow:

| Implication | Explanation |

|---|---|

| 1. High failure rate is priced-in | “Most will fail” = “most options expire at zero” — standard in option pricing. The real question: Is implied volatility (right-tail magnitude) sufficient to compensate risk? For frontier AI, the right tail is trillion-dollar companies — almost certainly yes. |

| 2. Asymmetric economics for founders vs. VCs | VCs hold diversified option portfolios — 1–2 wins cover all losses. Founders hold concentrated, illiquid positions with extreme downside. This explains talent flight: joining a Neolab demands belief in near-term, high-probability breakthroughs — not just brand appeal. |

| 3. Theta decay is the biggest threat | Options lose value over time. So do Neolabs. Every month without a paper, benchmark result, or working prototype erodes confidence, increases attrition risk, and shrinks right-tail probability. Success hinges on early validation — e.g., SSI’s silence is the highest-risk variant: either deliver a jaw-dropping product at launch… or collapse. |

3. Real Differentiation — Not Just GPT Clones

These aren’t copycat LLM shops. Their technical moats are distinct and defensible:

- Periodic Labs: Owns the world’s largest corpus of failed physical experiment data — a unique, non-replicable asset.

- World Labs: Betting on spatial intelligence and causal reasoning — prerequisites for robotics.

- Goodfire: Focused on mechanistic interpretability at frontier scale — a severe supply shortage.

- Liquid AI: Commercializing continuous-time neural networks, a credible Transformer alternative.

Their greatest value lies in uniqueness — but uniqueness alone doesn’t guarantee success.

Are Neolabs research labs? Startups? Product companies?

Answer: They are all three — simultaneously.

Historical analogs like Bell Labs or Xerox PARC were research arms of profitable parents — no funding pressure, no product deadlines, decades-long timelines. Yet they failed to capture commercial value from breakthroughs (transistors, GUI, Ethernet).

Neolabs cannot replicate that model. They must merge research rigor with startup velocity and product discipline — because value leaks when algorithm discovery and product delivery are siloed.

OpenAI proves it: GPT began as research — but became product because the same team owned both.

Yet tension remains:

🔹 Research rewards novelty, surprise, paradigm shifts — often taking years.

🔹 Product rewards speed, iteration, customer feedback, shipping.

Running both in a 20-person team requires extraordinary founder talent (Murati, Sutskever, Amodei) — or ends in fragmentation and mediocrity.

That structural difficulty — not market, talent, or capital — is the hidden reason most Neolabs will fail.

Six Emerging Neolab Paradigms

These 63 labs cluster into six strategic archetypes:

1. Frontier-General Labs

Thinking Machines Lab, SSI, Reflection AI, Humans&, AMI Labs, Recursive Superintelligence

Belief: AGI remains unclaimed territory. A lean, research-first team can outmaneuver incumbents via superior algorithms, smarter post-training, or open-weight foundations.

“Opaque APIs and giant teams aren’t the only path. Customizability, interpretability, and open weights enable asymmetric leaps.” — Mira Murati

2. Robotics & Embodied AI

Roze, Project Prometheus, Skild AI, Physical Intelligence, Rhoda AI, Genesis AI

Argument: Language is solved. Next frontier: acting in the physical world.

Roze’s edge? Not robots as products, but robots building AI infrastructure: data centers. With ~439K US construction workers missing, satellite imagery shows ~40% of AI data center projects delayed. If labor scarcity is structural, Roze may be the sole scalable solution.

3. AI for Science

Periodic Labs, Lila Sciences, Chai Discovery, Xaira Therapeutics, EvolutionaryScale, Isomorphic Labs, CuspAI

Premise: Web-scale text data is exhausted. Next breakthrough requires AI-driven autonomous physical experimentation — generating fresh, real-world data (especially unpublished failures).

Periodic Labs — co-founded by Liam Fedus (ex-OpenAI VP, ChatGPT co-creator) and Ekin Dogus Cubuk (ex-DeepMind Materials Lead) — raised $300M to build robotic labs that autonomously propose and run materials science experiments.

“Internet text is gone. Unpublished experimental failure data is the only ladder to physical models.”

4. World Models

World Labs (Li Fei-Fei), Decart, AMI Labs (Yann LeCun), General Intuition

Mission: Teach AI 3D spatial reasoning and causality — essential for robotics and real-world agency.

World Labs released Marble (2025) — a generative, explorable environment preview. AMI is testing LeCun’s decade-old JEPA framework at billion-dollar scale.

5. Frontier-Efficient / Architecturally Heterodox

Sakana AI, Liquid AI, Magic, Inception Labs, Ndea, Zyphra

Thesis: “Transformer everywhere” is a local optimum. If scaling laws plateau, labs pursuing alternate architectures will dominate the next decade.

- Liquid AI: Commercializing liquid foundation models (continuous-time neural nets)

- Sakana AI: Optimizing via evolutionary, compute-efficient methods

- Inception Labs: Diffusion-based language models

6. Verticalized Frontier Work

AxiomMath, Harmonic (formal math), Goodfire (interpretability), Inference (vLLM commercialization), Ricursive (chip-design AI), RadixArc (SGLang), QuTwo (quantum AI)

Argument: Going deep on one subproblem — formal proof automation, mechanistic interpretability, inference acceleration — yields deeper insights and stronger moats than generalist labs.

Three Forces Fueling the Neolab Surge

Force 1: Talent Exodus & Financial Liberation

2022–2024 created a generation of wealthy researchers. Anthropic’s ARR surged from ~$9B to $30B (2026); OpenAI hit ~$20B annualized revenue. Senior researcher equity packages reached 8–9 figures.

By 2025, many had achieved true financial independence — making entrepreneurship not self-actualization, but rational career optimization. Hence: Thinking Machines, AMI, Periodic, Reflection, Inflection.

Force 2: Sutskever’s Narrative Shift

In Nov 2025, Ilya Sutskever declared: “We’ve left the ‘scaling era’ and entered the ‘research era.’ Progress now depends more on new ideas than new GPUs — and frontier labs spend most compute on inference, not research.”

For fundraising researchers, this is gold: If progress is GPU-bound, you can’t beat OpenAI. If it’s idea-bound, a 30-person lab with the right insight can.

SSI’s existence — $32B valuation, zero product, zero roadmap — is the ultimate validation of this narrative.

Force 3: Dry Powder Meets Tiny Talent Pool

- Foundation Capital, a16z, Sequoia, Founders Fund, Khosla, Greenoaks, and sovereign funds launched dedicated AI funds in 2025.

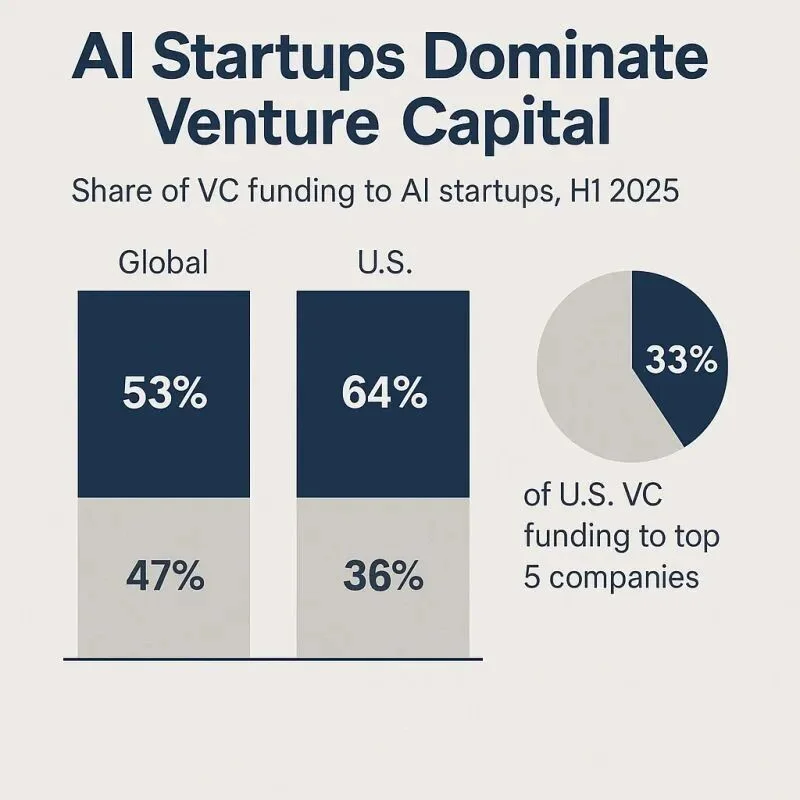

- US startup funding rose 76% YoY in H1 2025 ($162.8B), with AI capturing 64% of total deal value.

- Yet globally, < 1,000 people can lead frontier-scale model development.

Result? A capital-saturated, talent-starved market — where valuation reflects urgency to enter the category, not revenue expectations. For a four-person team, a $1B seed round isn’t price — it’s admission fee.

Geopolitical AI: Why the List Is So Localized

A striking macro trend: Geographic concentration is sharper in AI than in the internet era.

-

95% of Neolabs on this list are headquartered in San Francisco.

- A handful in Paris (AMI, H, Mistral-affiliated), London (Isomorphic), Tokyo (Sakana), Tel Aviv (AI21).

Internet-era innovation spread across NYC, Boston, Austin, Seattle, Berlin. Neolabs are crammed into ~25 square miles of California — creating intense competition for engineers, compute, office space, and investor attention — and driving R&D costs to astronomical levels.

Notably absent:

- Chinese labs (Moonshot, DeepSeek, Zhipu, MiniMax, Baichuan, 01.AI): Structurally distinct — backed by corporate VC (Alibaba, Tencent, ByteDance), government interfaces, different IP/data regimes, and hardware constraints. They prioritize engineering efficiency in application layers, not physics-defying “brute-force” research. Direct comparison misleads.

- Sovereign/mid-power labs: India’s Sarvam AI, Germany’s Aleph Alpha — excluded due to non-alignment with the “financially liberated ex-frontier-researcher” archetype, but represent a sovereign, multilingual, state-anchor model with potentially greater strategic scale.

- Hardware/infrastructure firms: Cerebras, Groq, Etched, Lightmatter — excluded as “non-model”, yet critical: if Etched’s Sohu chip delivers promised Transformer inference gains, every Neolab’s economics shift.

So What? Three Takeaways

1. For Investors

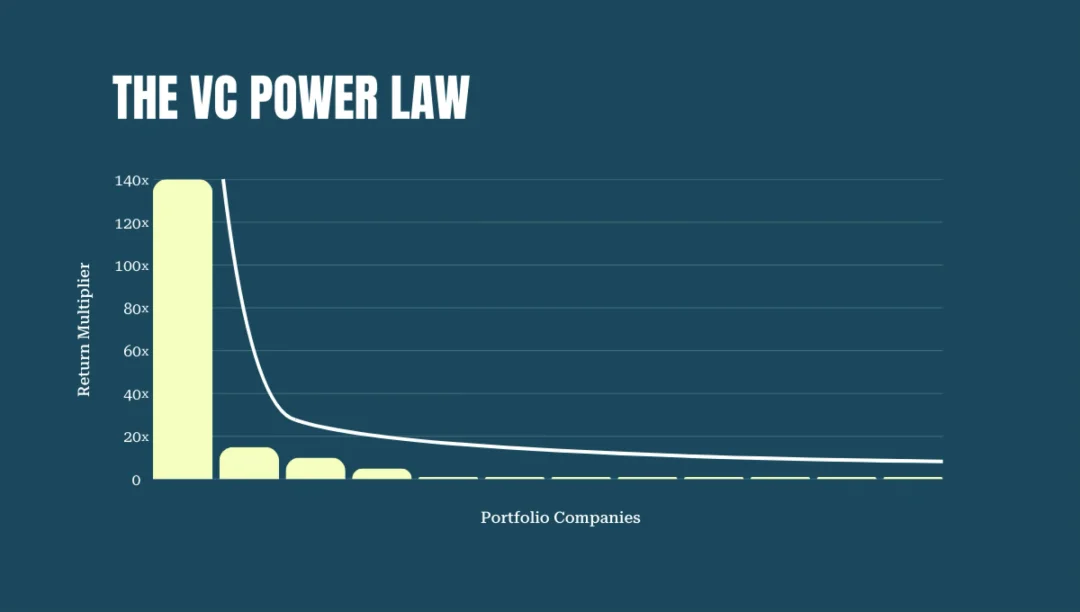

Treat Neolabs as an option book, not an equity portfolio. Expect massive dispersion:

– >90%: Fail to return capital

– 5–10%: Moderate exits

– 1–3%: Trillion-dollar outcomes

$30B aggregate valuation may be right — but distribution will differ wildly from Deedy’s 2026 list. Pick winners early, or index broadly — convexity in the right tail is extreme.

2. For AI Talent

Your career move is also an option trade. Joining a Neolab is high-variance, low-base-probability — justified only if you possess stronger conviction than the market about a specific direction’s right-tail potential and can bear total failure risk. Brand hype or peer pressure? A structurally flawed rationale.

Thinking Machines lost five founding members in <12 months. If you join for similar reasons, expect similar outcomes.

3. For Everyone Watching

Neolabs signal a field in profound transition. Incumbents haven’t won — if they had, talent wouldn’t flee and capital wouldn’t chase alternatives. But challengers haven’t proven themselves — no Neolab has matched OpenAI/Anthropic/DeepMind’s monthly output rhythm.

We’re mid-experiment: Will AI follow prior paradigms (few dominant winners)? Or something stranger — dozens of specialized labs, each dominating a vertical, with no single monopoly?

The most underrated possibility? AI evolves more like biotech than the internet.

Biotech built immense value through hundreds of specialized firms — none dominant, each owning a disease area or modality. If AI mirrors this — a vast, heterogeneous problem space demanding deep specialization, with no winner-take-all dynamic — then today’s Neolab valuations make sense even if no single firm hits $1T. And bearish “winner-take-all” arguments fail at first principles.

We don’t know yet — and that uncertainty is precisely what makes this list so compelling.

Article originally published by GGV Capital.