a16z Global AI Top 100: The Battle for AI Entry Points Intensifies — OpenClaw Ushers in the Universal Agent Era

Three years ago, we launched the first edition of this ranking with a simple goal: identify which generative AI products were truly adopted by mainstream consumers. At the time, the line between “AI-native” companies and others was starkly clear. ChatGPT, Midjourney, and Character.AI were built ground-up around foundational models — while the rest of the software industry was still experimenting with how to integrate the technology.

That boundary has dissolved. CapCut — a video editor with 736 million monthly active users — relies on AI for its most popular features: background removal, AI effects, auto-captions, and text-to-video. Canva’s entire growth engine runs on its Magic Suite AI tools. Notion’s paid AI adoption surged from 20% to over 50% in one year — AI now accounts for roughly half of the company’s ARR.

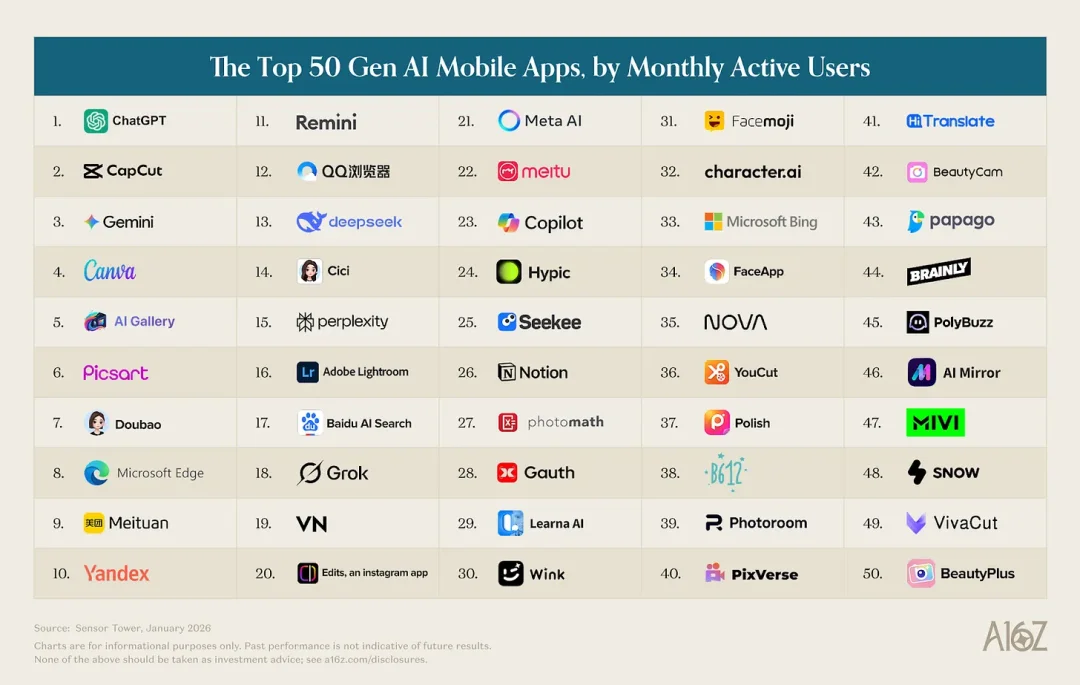

Starting with this edition, we’ve expanded our scope to include any consumer product that embeds generative AI as a core part of the experience — including CapCut, Canva, Notion, Picsart, Freepik, and Grammarly. This better reflects how people actually use AI today — though AI-native products still dominate the top ranks.

As always, our web rankings are based on monthly unique visitors (SimilarWeb, data through January 2026); mobile rankings reflect monthly active users (Sensor Tower, data through January 2026).

01 ChatGPT Leads — But the “Default AI” War Has Begun

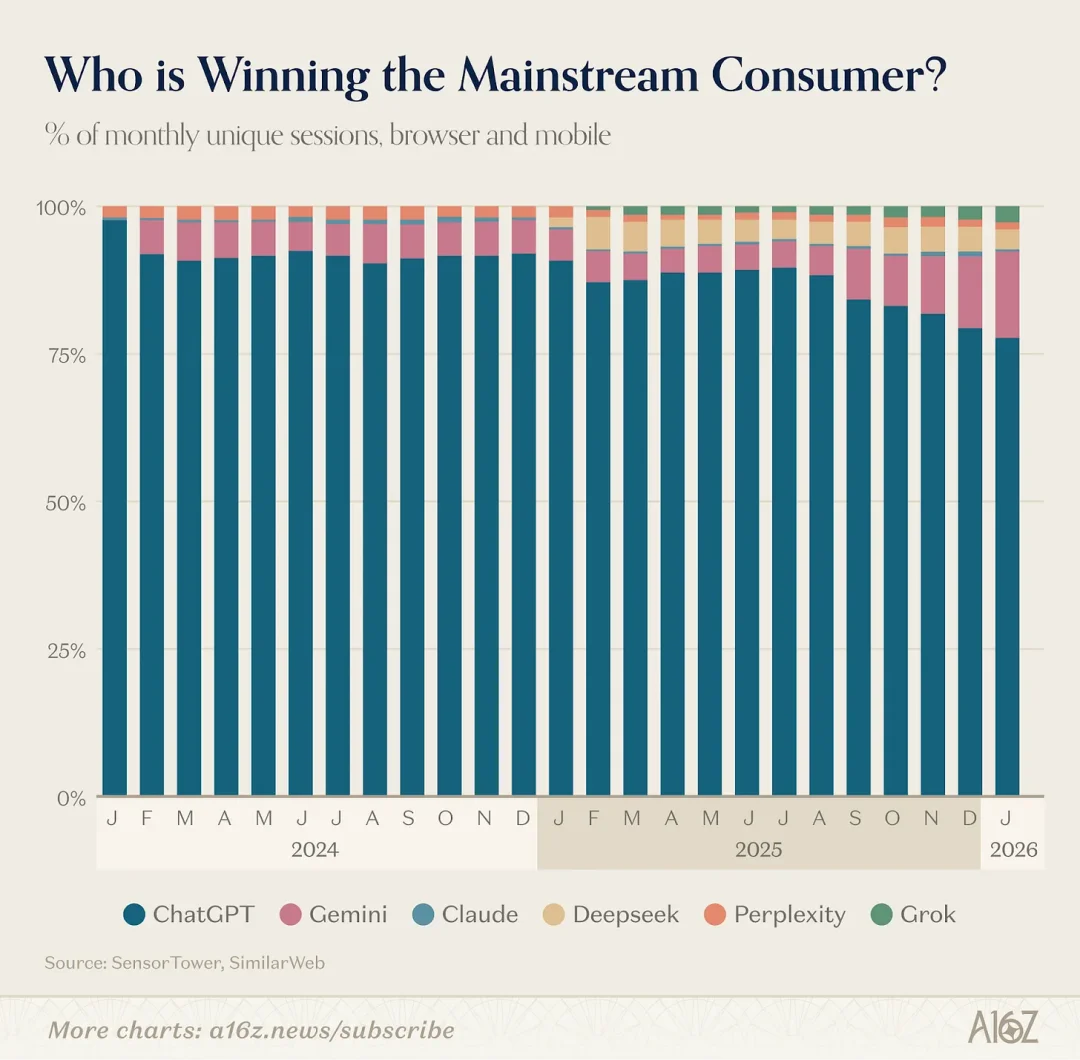

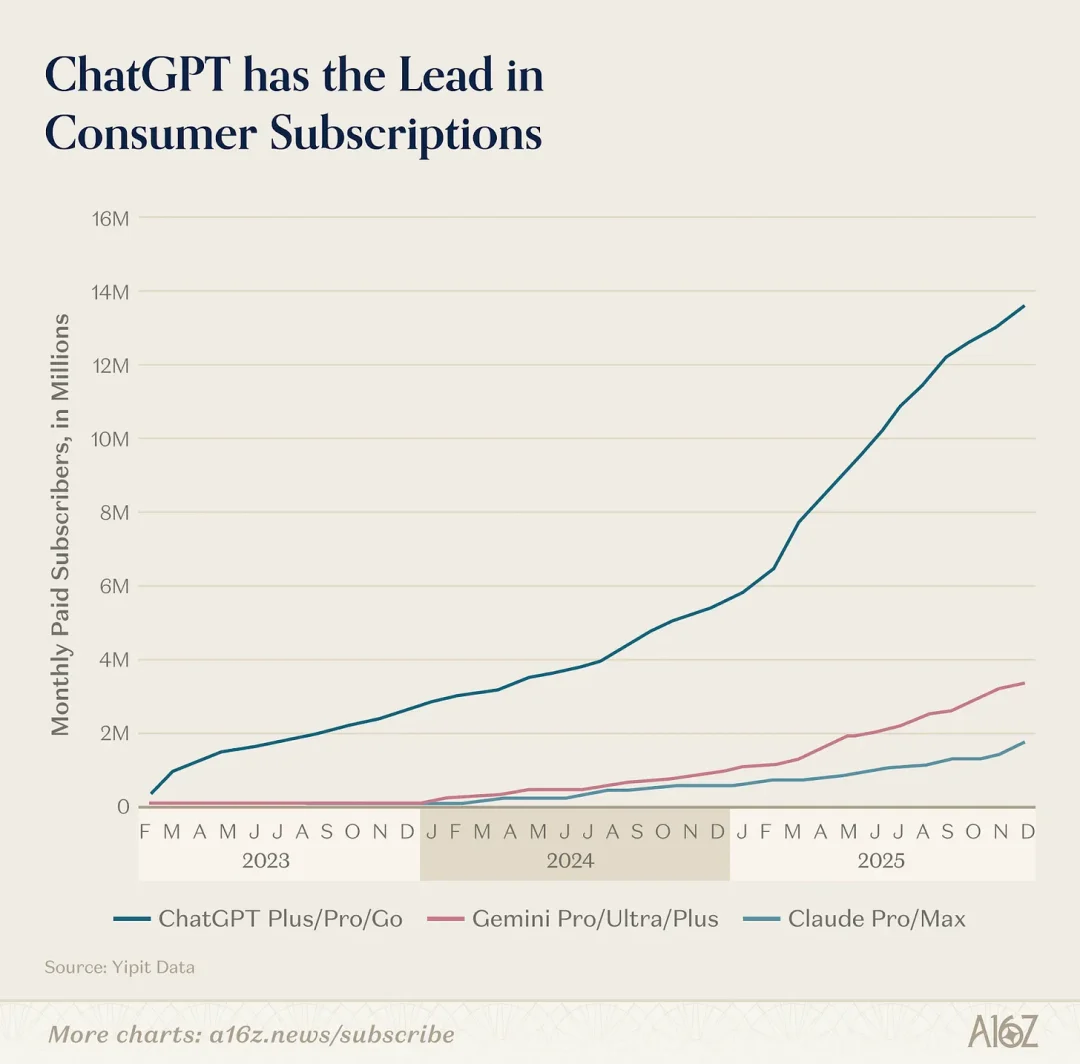

ChatGPT remains the undisputed leader among consumer AI products. On the web, its monthly traffic is 2.7× greater than Gemini’s; on mobile, its MAUs are 2.5× higher. Its weekly active users grew by 500 million over the past year — reaching 900 million today, meaning >10% of the global population uses it weekly. Maintaining such growth at this scale is extraordinary.

Yet the field is broadening. Gemini and Claude are accelerating their US paid subscription growth — though still far behind ChatGPT (Claude: 1/8th, Gemini: 1/4th). Per Yipit Data (Jan 2026), Claude’s paid subs grew >200% YoY, Gemini’s 258%. Crucially, multi-platform usage is rising: ~20% of ChatGPT’s weekly web users also used Gemini in the same week.

Competitors are sharpening their focus: Google launched Nano Banana (200M images in Week 1 → +10M new Gemini users) and Veo 3 — widely hailed as a breakthrough in AI video. Anthropic doubled down on pros: Cowork, Claude-in-Chrome, Excel & PowerPoint plugins, and the standout — Claude Code.

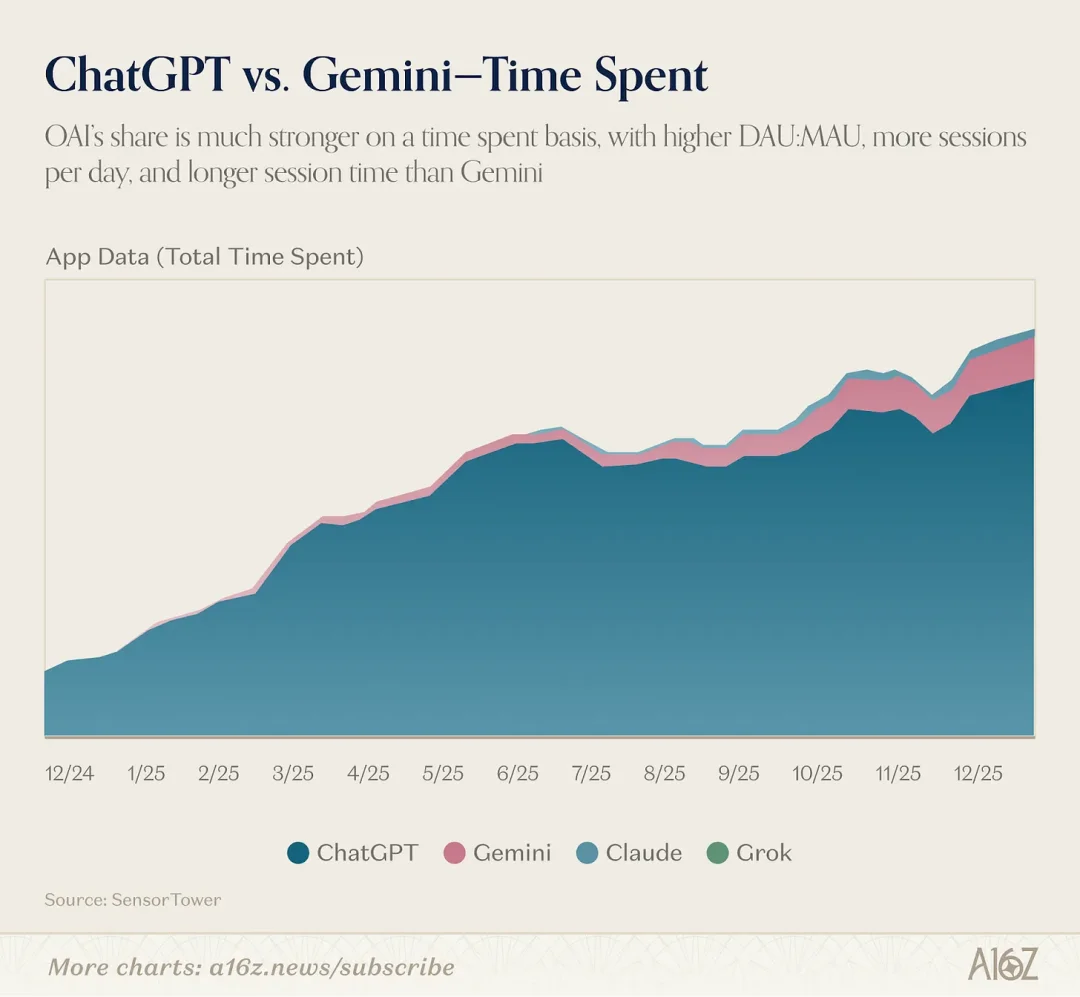

The real stakes? Irreplaceability. Context compounds: the more an LLM learns about you, the better its output — and the stickier your usage. Early data shows Gemini’s web sessions per user are rising — yet ChatGPT still leads by 1.3×. On mobile, ChatGPT holds a 2.2× advantage in monthly sessions per user. Both maintain industry-leading subscription retention in the US.

A second lock-in layer emerges via app ecosystems. ChatGPT (GPTs, Apps) and Claude (MCP integrations, Connectors) let users build workflows atop assistants. Once you connect calendars, email, and CRMs, switching costs soar — and developers naturally concentrate on the largest platforms, fueling a classic flywheel.

Strategic divergence is evident:

– OpenAI aims to “bring AI to billions who can’t afford subscriptions” — hence ads and the upcoming “Sign in with ChatGPT” identity layer, positioning the assistant as the default interface to the internet: shopping, bookings, health, daily life.

– Anthropic targets AI power users (developers, knowledge workers), betting on high-value subscriptions.

App directories reveal the split: As of late February, ChatGPT’s App Store hosts 220 apps across 13 categories; Claude offers ~160 curated connectors + ~50 community MCP servers. Only 41 apps overlap (~11%), mostly universal productivity staples: Slack, Notion, Figma, Gmail, Google Calendar, HubSpot, Stripe.

Beyond this core, they diverge radically:

– ChatGPT: 85+ apps in travel, shopping, food, health, lifestyle, and entertainment — transactional domains: Expedia flights, Instacart groceries, Zillow listings, MyFitnessPal nutrition tracking. This is the most aggressive super-app strategy in AI.

– Claude: Exclusive integrations in finance (PitchBook, FactSet), dev infra (Sentry, Supabase, Snowflake), science/medicine (PubMed, Clinical Trials, Benchling), and a thriving open-source MCP ecosystem — absent from ChatGPT.

If AI assistants evolve into OS-level environments, this may mirror the mobile OS wars — not search dominance (90% share), but two distinct trillion-dollar ecosystems.

02 Fragmentation, Not Monopoly: Three Global AI Ecosystems

Geographically, AI markets are splitting into three distinct, widening ecosystems.

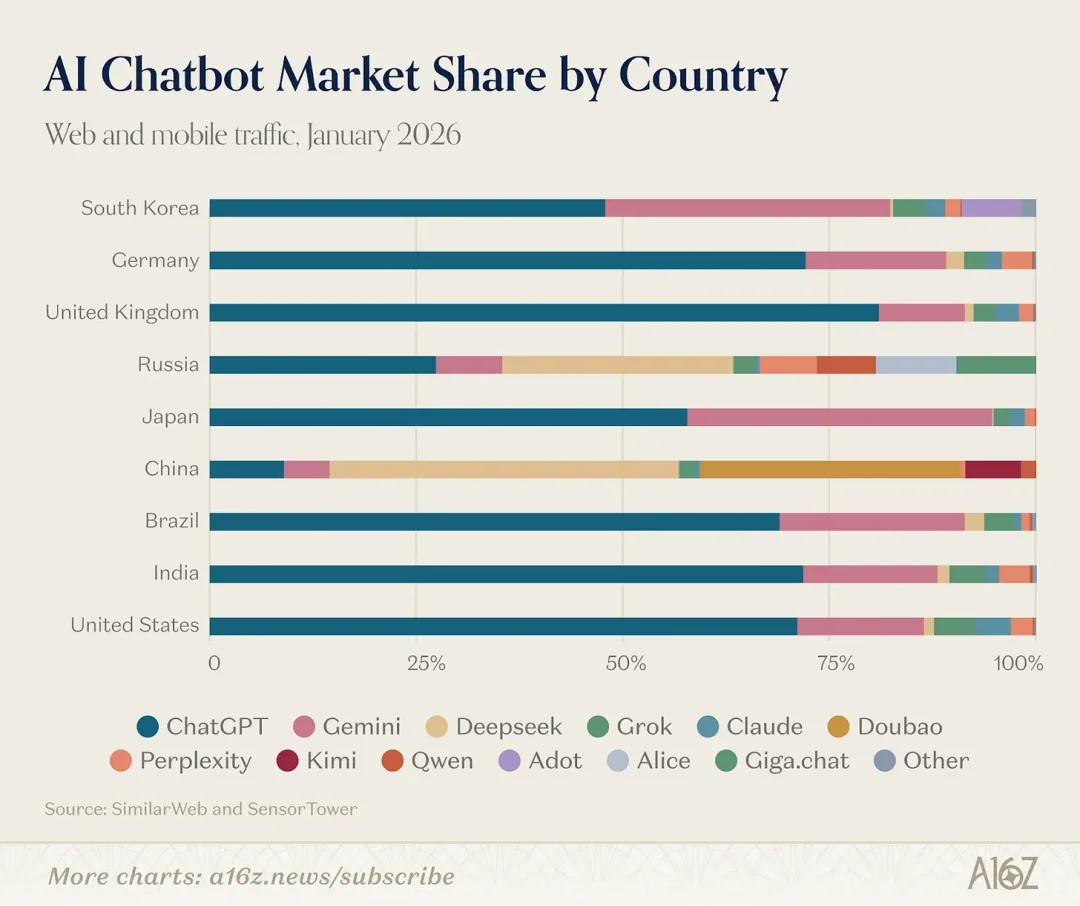

Western AI tools share highly overlapping user bases: ChatGPT, Claude, Gemini, and Perplexity all draw top traffic from the same pool — US, India, Brazil, UK, Indonesia — differing only in rank order. None hold significant traction in China or Russia, due to policy: Western sanctions restrict Russian access since 2022; China mandates registration, data localization, and content compliance.

DeepSeek is the sole cross-border outlier: 33.5% of its web traffic comes from China, 7.1% from Russia, 6.6% from the US — similar patterns hold on mobile. Chinese users also heavily adopt ByteDance’s Doubao and local model Kimi.

Russia has evolved into a third pole: DeepSeek ranks #2 globally in penetration. Yandex Browser — integrated with Alice AI — hit 71M MAUs, landing in the global mobile AI Top 10. Sber’s GigaChat debuted on our web list. Like China, sanctions created a vacuum — filled by domestic players in under two years.

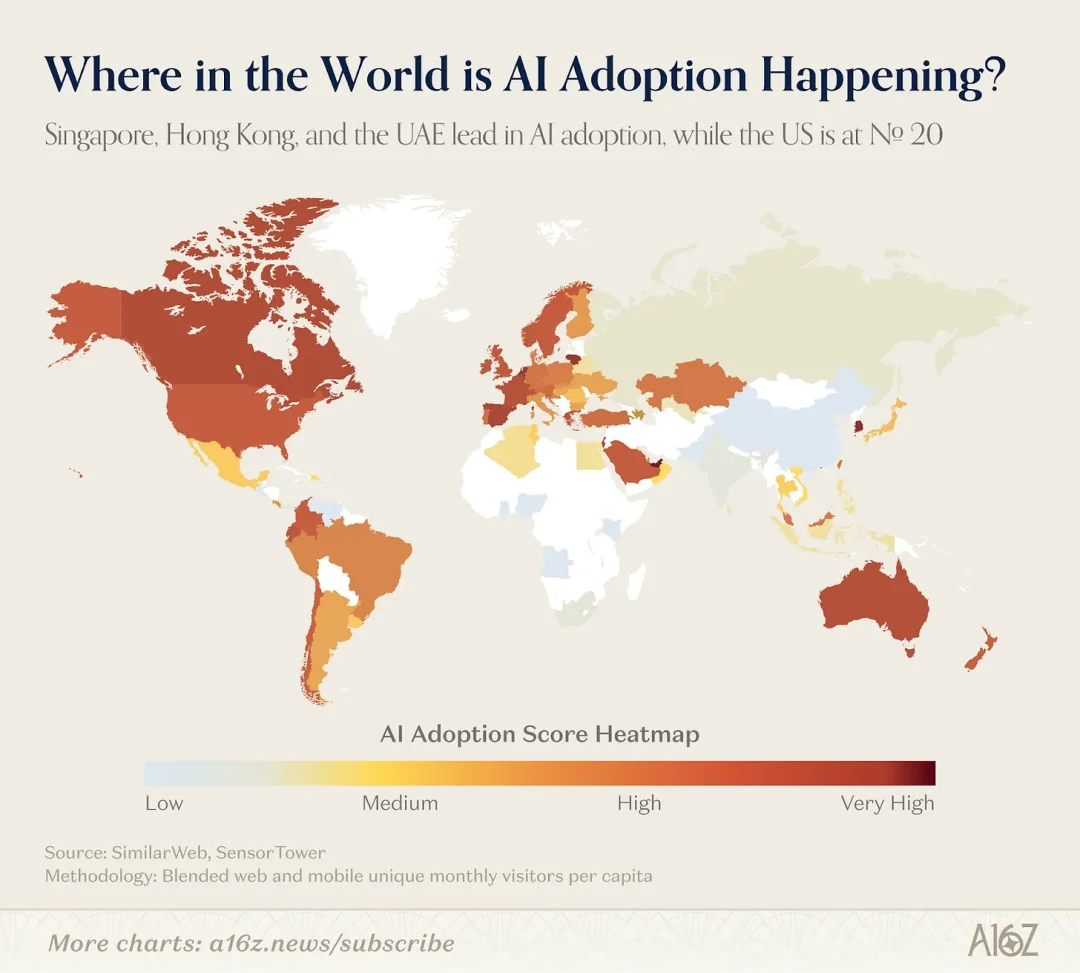

To gauge per-capita AI adoption, we built an index (0–100) combining per-capita web visits and mobile MAUs. Results reshaped the map: Singapore leads, followed by UAE, Hong Kong, and South Korea. The US — home to most of these products — ranks #20.

03 Giants Invade Image & Video — Independent Creators Pivot

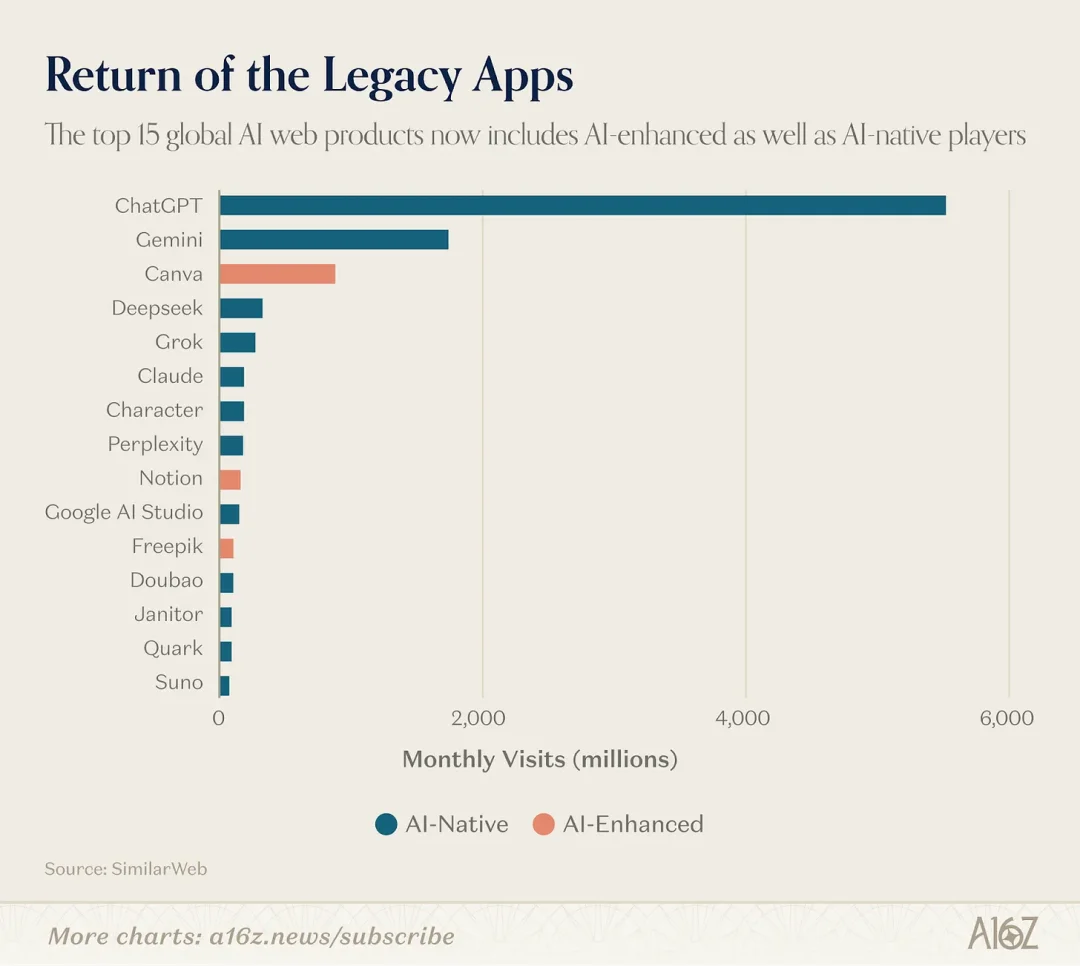

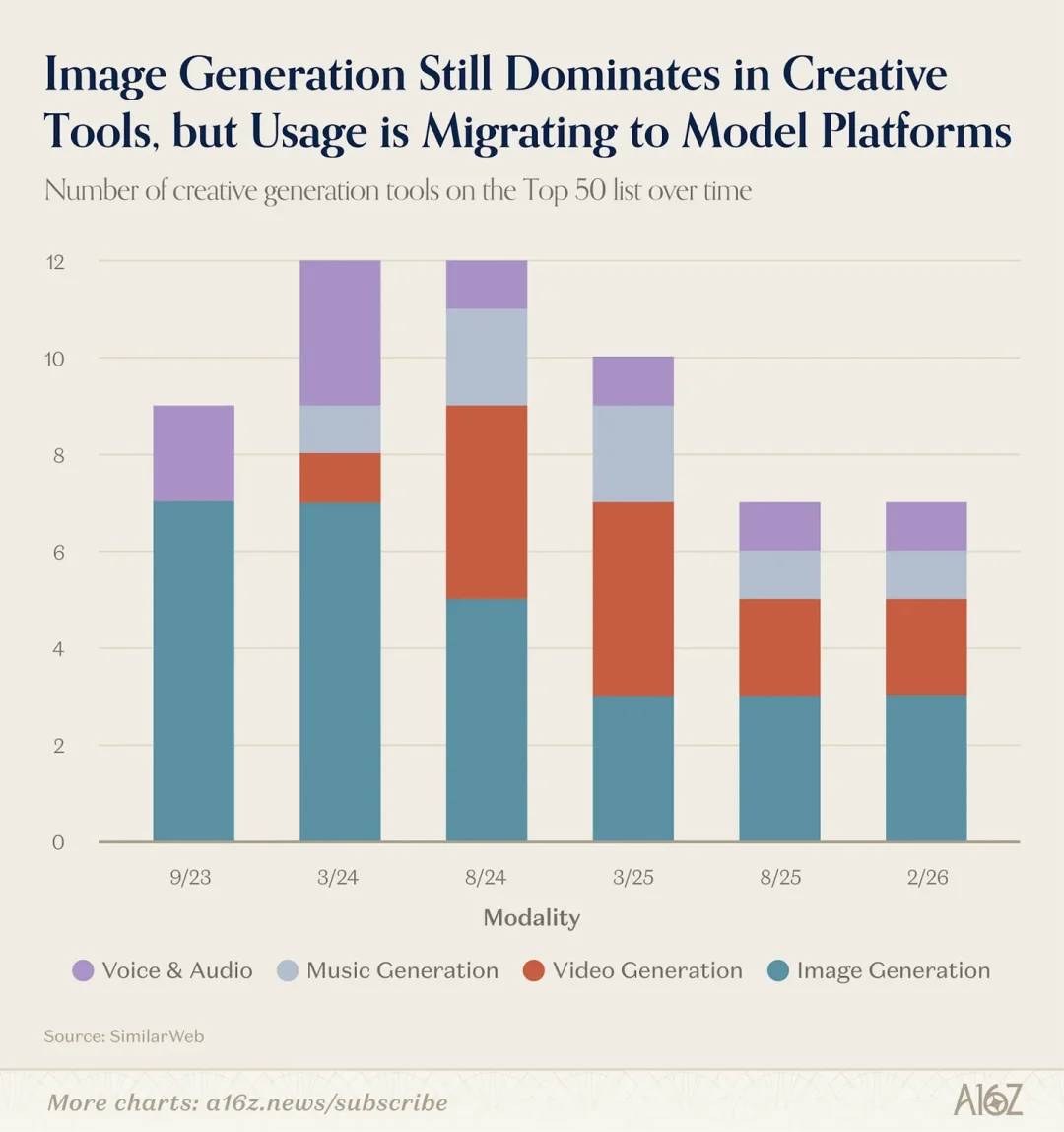

Midjourney, DALL-E, and Stable Diffusion introduced early users to generative AI — all pre-dating ChatGPT. Image generators dominated creative tools (video/audio arrived later) and anchored our first three lists. That landscape has shifted dramatically.

In the September 2023 debut, 7 of 9 web-based creative tools were image generators. Three years later, only 3 remain — yet 7 creative tools still rank. The gap was filled by video, music, and voice products.

The image story is consolidation. As ChatGPT’s GPT Image 1.5 and Gemini’s Nano Banana matured, standalone image tools faced soaring quality thresholds. Midjourney fell from Top 10 to #46. Survivors — Leonardo, Ideogram, CivitAI — serve niche creative communities with distinctive, opinionated features — rather than competing on general capability.

Video generation is this edition’s most volatile segment. Kling AI (Kling), Hailuo (Hailuo), and Pixverse (Aish) built real user traction. China-developed models continue leading on output quality — Seedance 2.0-powered apps may appear next edition. Veo 3 was Google’s first major catch-up model, lifting Google Labs’ rank from #36 to #25.

Sora is absent — but not irrelevant. OpenAI launched Sora 2.0 as a standalone app in Sept 2025: users upload digital avatars (“Cameos”) for human-in-the-loop video. It topped the US App Store for 20 days — faster than ChatGPT’s initial download surge. Yet viral social adoption stalled (no AI × social loop emerged), excluding it from this mobile list. SensorTower confirms >3M DAUs — creators actively use it, even if sharing elsewhere.

Music & voice remain defensible. Suno (#15) held its rank; ElevenLabs has ranked every edition since Sept 2023 — its specialized capabilities (voice cloning, dubbing, audio production) haven’t been commoditized as bundled features.

Pattern: Where giants (Google, OpenAI) concentrate R&D (images, increasingly video), independent tools face traffic compression — yet space remains for differentiated, niche, monetizable offerings. Where giants don’t compete (music, voice), independence thrives.

04 Universal Agents Arrive: OpenClaw Signals a New Paradigm

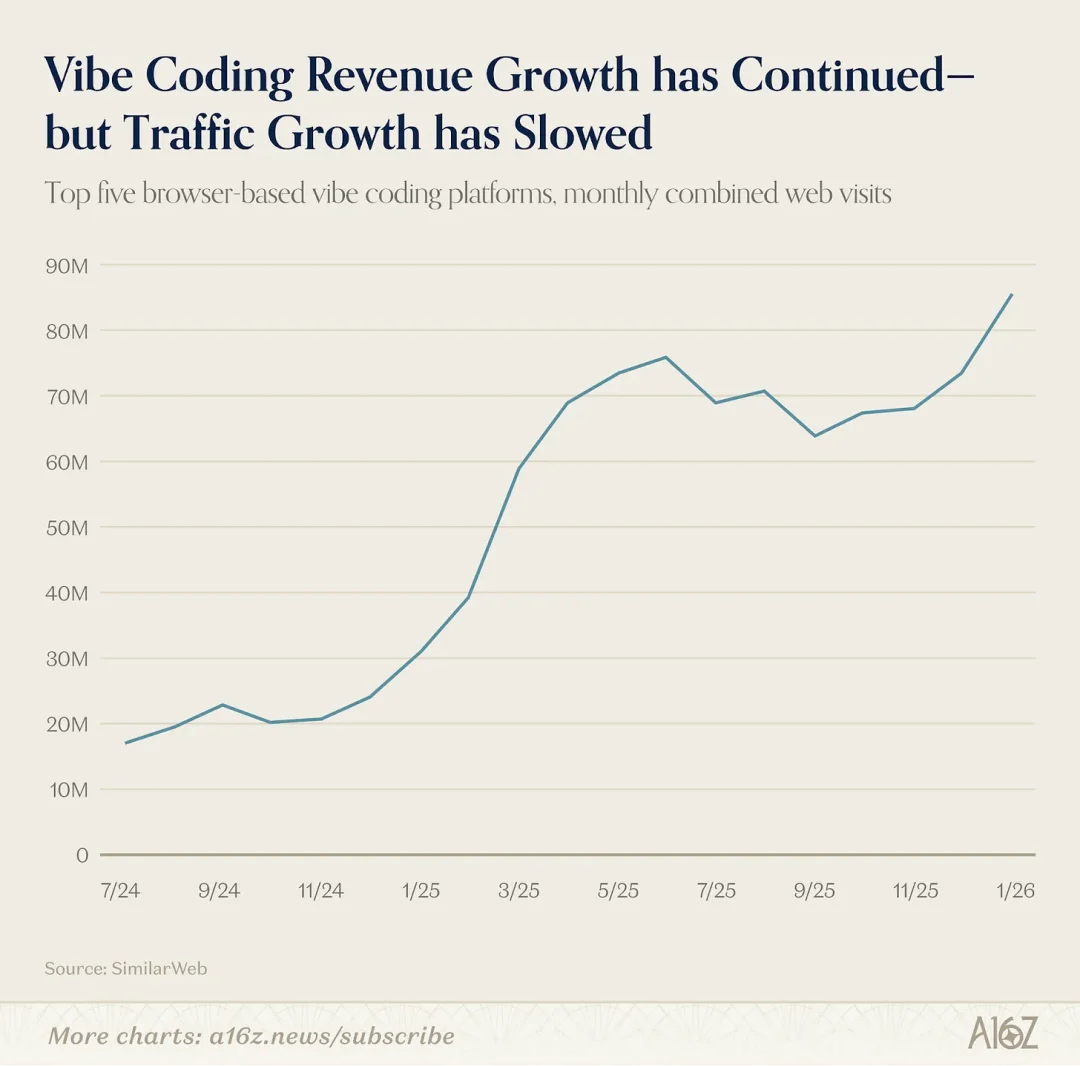

The shift toward agent-style AI began last edition with Vibe Coding. When Lovable, Cursor, and Bolt appeared on the March 2025 list, they represented something novel: AI products that build things — not just answer questions or generate media. That’s vertical-specific agents.

Vibe Coding proved sticky with technical users — Replit and Lovable return this edition; so does Claude Code (via Claude). Growth continues, though velocity has moderated. Revenue rises as developer teams deepen usage.

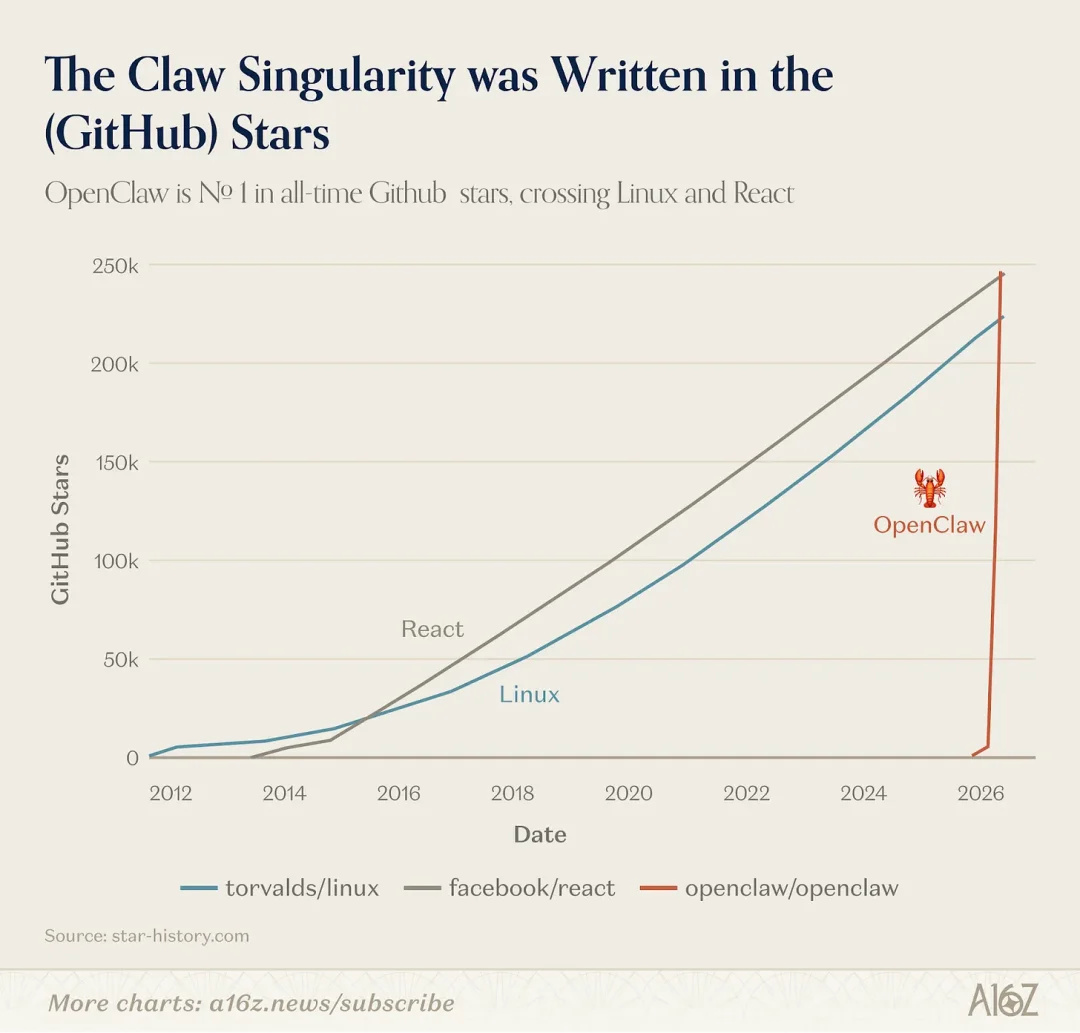

Now, universal agents are emerging. In January 2026, Austrian developer Peter Steinberger’s open-source project OpenClaw exploded: from hobbyist experiment to 68,000 GitHub stars in weeks, earning mainstream coverage. OpenClaw is a locally-run AI agent that connects to messaging apps (WhatsApp, Telegram, Signal) and executes multi-step tasks autonomously.

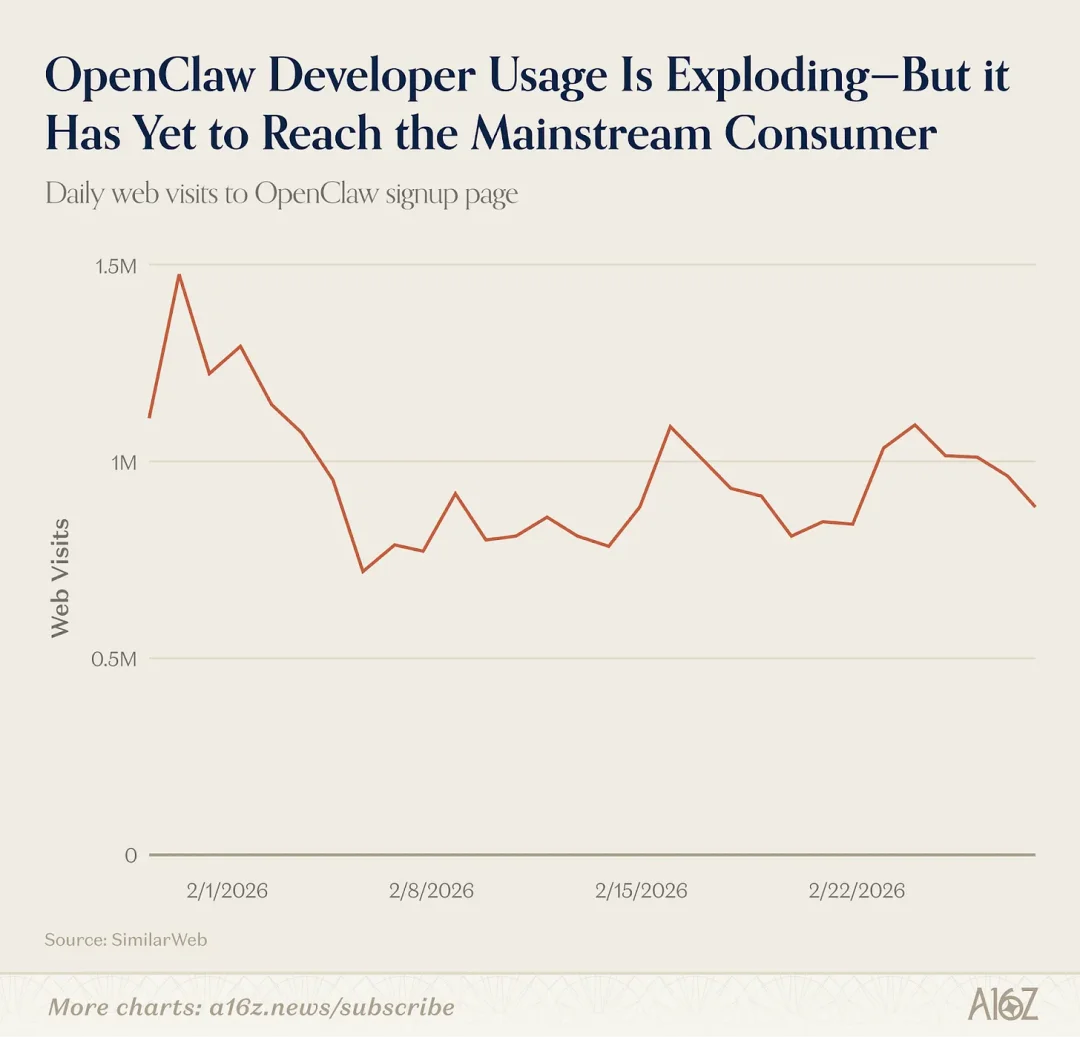

If ChatGPT taught consumers AI could speak, OpenClaw may be the moment they realize AI can act. It ignited developer communities — had analysis extended to February, OpenClaw would rank Top 30 on web.

But OpenClaw isn’t consumer-ready: installation requires terminal fluency. Its growth among tech users continues — it recently surpassed React and Linux as GitHub’s #1 starred project. Yet “graduation” to mass adoption remains elusive (new install-page traffic is flat). Its acquisition by OpenAI in Feb 2026 hints at a forthcoming, simplified version.

OpenClaw isn’t alone: Manus (ranked again; acquired by Meta for ~$2B in Dec 2025) and Genspark (new entrant; $300M Series B, $100M ARR) also enable open-ended task execution — research, spreadsheet analysis, slide creation — end-to-end.

On mobile, interaction often happens via messaging: users message OpenClaw like a friend, and it acts silently in the background. Poke offers similar SMS-based agent experiences.

These will compete directly with universal LLM assistants (ChatGPT, Claude, Gemini) as they add connector-driven agent capabilities. Will consumers pick one primary agent — or fragment across use cases? The next six months will decide.

05 AI Is Leaving the Browser: From Destination to Embedded Function

Past editions ranked AI products solely on web traffic and mobile MAUs. A new class of AI products — growing rapidly — evades both metrics.

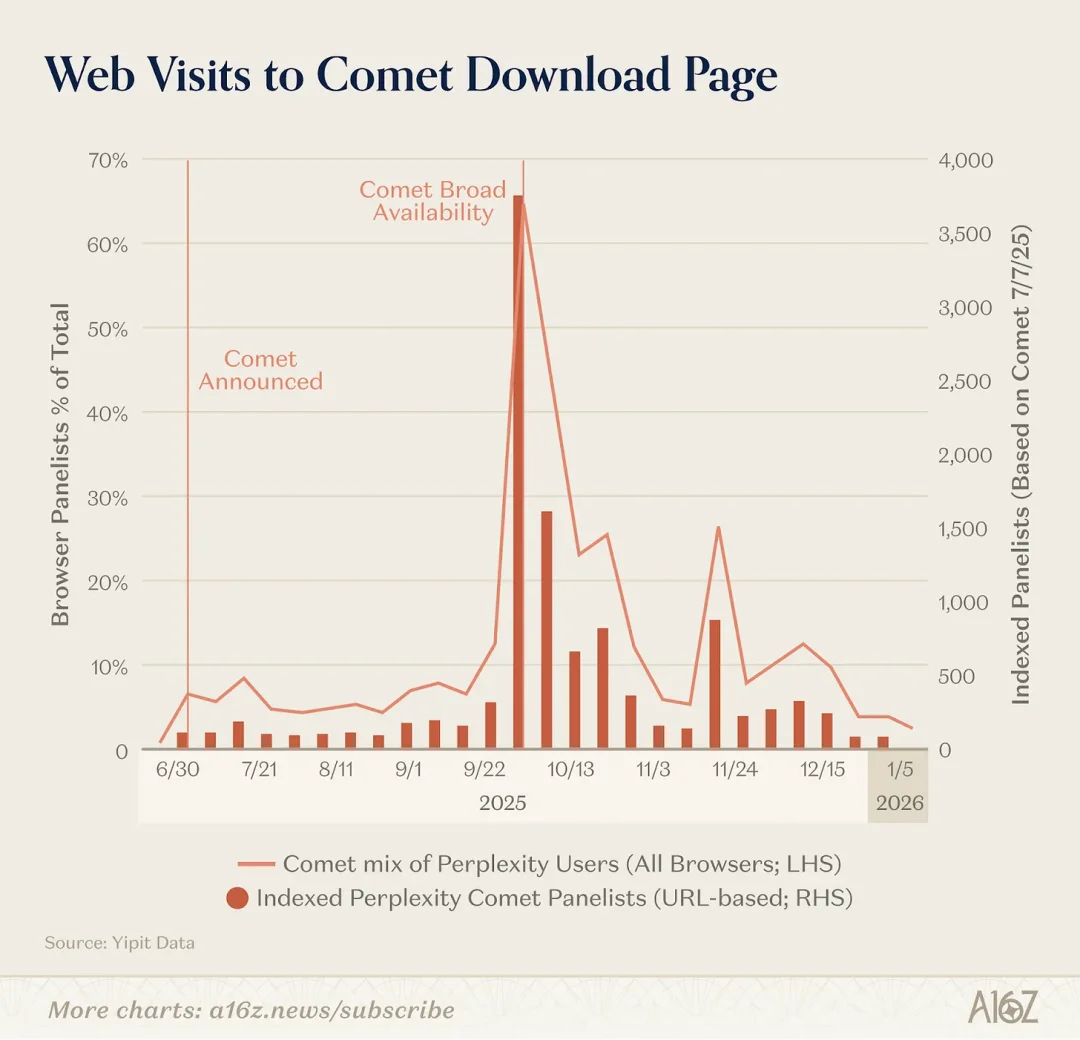

The most visible shift: browsers themselves becoming AI products. In the last nine months: OpenAI launched Atlas (Chrome-like browser with ChatGPT on every page); Perplexity released Comet; Browser Company (acquired by Atlassian) debuted Dia. Perplexity’s Comet generated the strongest initial download impact — but no AI browser shows accelerating growth yet.

Other giants embed AI into existing browsers: Google added Gemini to Chrome and launched Disco (dynamic web-app generator); Anthropic rolled out Claude-in-Chrome, connecting to user sessions to drive on-page actions.

Desktop-native AI tools show explosive growth — especially for developers. Claude Code (CLI agent) hit $1B ARR in six months. OpenAI’s Mac-only Codex app reached 2M WAUs by early March, growing 25% weekly. Cursor remains in the web Top 50.

For mainstream consumers, AI desktop apps center on voice: Fireflies, Fathom, Otter, TL;DV, and Granola (meeting transcription tools) acquire users via PLG and penetrate enterprises — collectively hitting 20M visits. Workspace apps like Notion (first-time entry this edition) integrate AI via transcription, research agents, and automation.

Finally, AI is embedding deeply into everyday tools:

– Anthropic: Claude-in-Excel & Claude-in-PowerPoint

– OpenAI: ChatGPT-for-Excel

– Google: Gemini in Docs, Sheets, Gmail, Meet — plus Personal Intelligence (Jan 2026), linking Gemini to Gmail, Photos, YouTube, and Search to reference hotel bookings, purchases, photos, and watch history — without prompting.

Implication for this ranking: Our methodology increasingly fails to capture the AI tools people use most. A developer spending 8 hours/day in Claude Code, or a knowledge worker dictating every email via Wispr, are heavy AI users — yet leave almost no trace in web traffic data. As AI shifts from destination to function, our measurement must evolve too.

Article sourced from Founder Park.